The BrahMos supersonic cruise missile has been one of India’s most lethal arms exports. (File photo)

The BrahMos supersonic cruise missile has been one of India’s most lethal arms exports. (File photo)

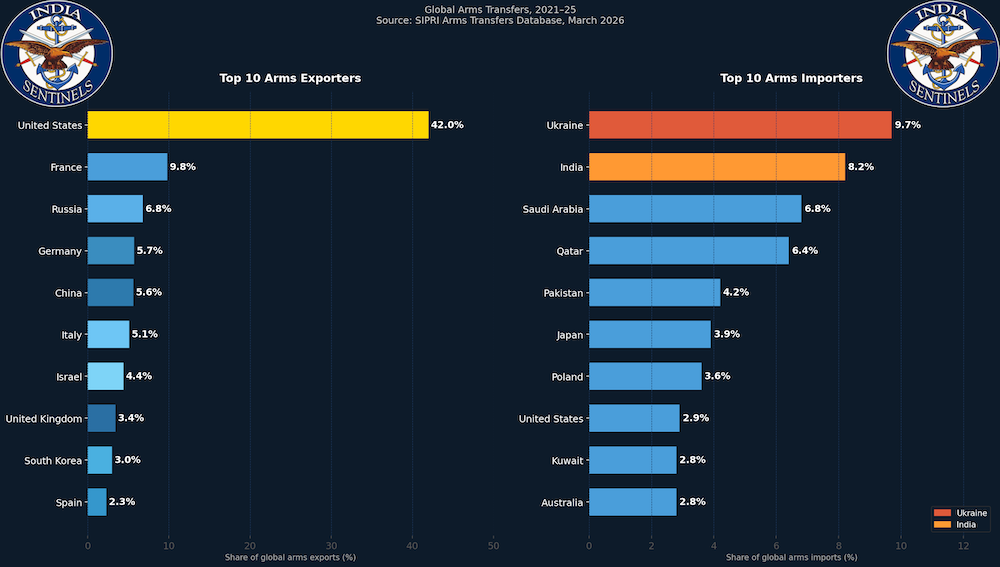

New Delhi: The volume of major arms transferred between states reached its highest level in more than a decade in 2021–25, rising 9.2 per cent compared with the previous five-year period (2016–20), according to the Stockholm International Peace Research Institute (Sipri), which released its annual arms transfers fact sheet [archived link] on Monday. The uptick – the steepest since 2011–15 – was driven primarily by Europe’s war-driven rearmament and a surge in demand from the Middle East and East Asia.

The five largest suppliers in 2021–25 were the United States, France, Russia, Germany and China, which together accounted for 70 per cent of all global arms exports. On the import side, the five largest recipients were Ukraine, India, Saudi Arabia, Qatar, and Pakistan – a list that reflects the geography of active conflicts and strategic anxieties as much as any formal procurement doctrine.

Top 10 arms exporters and importers by share of global transfers, 2021–25. (Source: SIPRI Arms Transfers Database, March 2026)

Top 10 arms exporters and importers by share of global transfers, 2021–25. (Source: SIPRI Arms Transfers Database, March 2026)

India: Still second-largest buyer, but Russian link frays

India retained its position as the world’s second-largest recipient of major arms in 2021–25, with an 8.2 per cent share of total global imports – even as its actual import volume dipped 4 per cent compared with 2016–20. The decline is partly a consequence of India’s push to indigenize defence production, though Sipri notes that domestic programmes often run years behind schedule.

The more consequential shift is in who supplies India. Russia, which accounted for 70 per cent of Indian arms imports in 2011–15, has seen its share fall to 51 per cent in 2016–20 and further to 40 per cent in 2021–25. France is now the second-largest supplier (29 per cent), and Israel the third (15 per cent), while the US has also gained ground. The diversification reflects both strategic hedging and frustration with delays in Russian deliveries, compounded after Moscow redirected defence production to sustain its war in Ukraine.

Future orders signal an accelerating westward tilt. India has placed or is in advanced negotiations for up to 140 Rafale combat aircraft from France – beyond the 36 already in service – and six submarines from Germany. Meanwhile, India’s own Tejas-Mk1A programme, the light combat aircraft (LCA) built by Hindustan Aeronautics Limited (HAL), aims to reduce import dependency in the fighter segment, though the pace of deliveries remains a subject of debate within the defence establishment.

Arms procurement in India is driven, in large part, by its unresolved borders with both China and Pakistan. That calculation came into sharp relief in May 2025, when a brief but significant military confrontation between India and Pakistan saw both sides deploy imported major arms, Sipri noted.

Pakistan: Deeper inside China’s orbit

Pakistan moved from the 10th-largest arms importer in 2016–20 to the fifth largest in 2021–25, as its purchases surged 66 per cent. China is now the dominant supplier, accounting for 80 per cent of Pakistani arms imports – up from 73 per cent previously. The defence partnership spans combat aircraft, frigates, submarines, and missile systems. Türkiye (Turkey) has also emerged as a notable secondary supplier (7 per cent), which reflects Islamabad’s effort to broaden its procurement base, albeit within a China-centric framework.

China: Arming others more, buying less

China’s role in global arms trade is increasingly that of exporter rather than importer. Its arms imports fell 72 per cent between 2016–20 and 2021–25 – one of the steepest declines among major powers – as the People’s Liberation Army relies more heavily on domestically built platforms. China dropped out of the world’s top 10 arms importers for the first time since 1991–95.

On the export side, China ranked fifth globally (5.6 per cent share). However, the concentration of its exports is striking: 61 per cent went to Pakistan alone. Serbia (6.8 per cent) and Thailand (4.7 per cent) were the next-largest recipients. China supplied arms to 47 states in the period, primarily in Asia, Oceania and Africa.

Europe remilitarizes, Ukraine tops import charts

In a shift not seen since the 1960s, Europe in 2021–25 became the region with the largest share of global arms imports – 33 per cent – overtaking Asia and Oceania (31 per cent) and the Middle East (26 per cent). Russia’s full-scale invasion of Ukraine in February 2022 triggered the most rapid European rearmament since the Cold War.

Ukraine was the world’s single largest arms recipient in 2021–25, absorbing 9.7 per cent of total global imports – compared with a negligible 0.1 per cent in 2016–20. At least 36 states supplied it with major arms. The US was the largest donor (41 per cent of Ukraine’s imports), followed by Germany (14 per cent) and Poland (9.4 per cent). However, US transfers dropped substantially in 2025 after the Trump administration scaled back military aid, leaving European states, Australia and Canada to fill much of the gap.

Arms imports by the 29 current European Nato member states grew 143 per cent between the two periods. Poland stood out as the continent’s most aggressive rearmament story: its imports were more than nine times higher (+852 per cent), with 47 per cent sourced from South Korea and 44 per cent from the US. Seoul has become one of the surprise winners of Europe’s defence spending surge.

US arms exports: Bigger than next seven combined

The United States increased its arms exports 27 per cent between 2016–20 and 2021–25, lifting its share of global exports to 42 per cent – more than the next seven largest suppliers combined. It exported to 99 states. For the first time in two decades, Europe (38 per cent) displaced the Middle East as the primary destination of US arms exports. Saudi Arabia was the single largest individual recipient (12 per cent), followed by Ukraine (9.4 per cent) and Japan (8.9 per cent). Twelve European states had a cumulative 466 F-35 combat aircraft on order or pre-selected for order by end-2025.

Russia’s collapse in global arms market

Russia’s arms exports fell 64 per cent, dropping its global market share from 21 per cent to 6.8 per cent. It was the only country among the world’s top 10 suppliers to record a decline. Cancellations and delivery failures to Algeria, Egypt, and other longstanding clients – driven by diversion of military materiel to the Ukraine front – were the primary cause. Nearly three-quarters of Russian exports in 2021–25 went to India (48 per cent), China (13 per cent) and Belarus (13 per cent).

Middle East, Africa and the wider world

Arms imports to the Middle East fell 13 per cent overall, yet the region still accounted for 26 per cent of global imports. Saudi Arabia (rank 3), Qatar (rank 4) and Kuwait (rank 9) were the top three importers. More than half of Middle Eastern arms imports came from the United States (54 per cent). Kuwait’s imports surged over nine times (+805 per cent), as it took delivery of 28 combat aircraft and 218 tanks from the United States and 23 combat aircraft from Italy.

Israel, despite growing international censure over civilian casualties in Gaza, continued to receive arms throughout 2021–25. Its imports rose 12 per cent, with the US supplying 68 per cent and Germany 31 per cent. Israel also climbed to seventh-largest arms exporter globally, with a 56 per cent rise in exports driven by demand for its air-defence systems. Iran’s only arms supplier in 2021–25 was Russia.

In Africa, overall arms imports fell 41 per cent. In sub-Saharan Africa, the Sudanese civil war that began in April 2023 drew arms from at least five identified suppliers to the government forces; the opposing Rapid Support Forces received deliveries from unknown sources.

Japan’s imports jumped 76 per cent as it expanded military capability in response to a more assertive China and North Korea. South Korea, by contrast, cut imports 54 per cent as its own defence industry expanded – it is now the ninth-largest arms exporter globally.

Note: Sipri’s data covers actual deliveries of major arms as defined by its trend-indicator value (TIV) methodology. Five-year averages are used to smooth year-on-year fluctuations. The SIPRI Arms Transfers Database, updated on March 9, 2026, covers transfers from 1950 to 2025.

Follow us on social media for quick updates, new photos, videos, and more.

X: https://x.com/indiasentinels

Facebook: https://facebook.com/indiasentinels

Instagram: https://instagram.com/indiasentinels

YouTube: https://youtube.com/indiasentinels

© India Sentinels 2026-27